That is the question that the Supreme Court last week agreed to consider in a case (South Dakota v. Wayfair, Inc., et al) that will have national implications for online retailers as well as brick and mortar businesses.

The Supreme Court had previously held that states could only tax a merchant’s sales if that business had a physical presence within the state. A physical presence could mean a warehouse, a distribution center, or an office. This previous line of cases, decided between 1967 and 1992, generally involved mail-order sales in the pre-internet era.

Since then, online sales have proliferated and are consuming an ever-increasing share of total retail sales. This has negatively affected both state finances and brick and mortar businesses. States rely on consumption taxes, like sales tax, to help fund government operations. With more online sales, that means less tax money. Brick and Mortar businesses are hit twice as hard. First, they pay to have products shipped to a physical location within the state which raises prices (consumers usually pay for shipping separately in online sales), and second, because brick and mortar businesses have that physical presence, they have to charge their customers sales tax. However, consumers love it because they are saving money.

Which brings us to South Dakota.

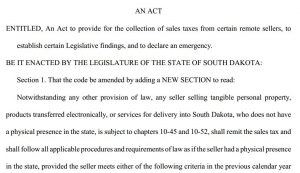

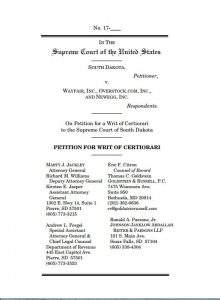

South Dakota estimated its tax loss related to online sales at upwards of $50 million dollars per year. In response, South Dakota passed a lawin 2016 that required online merchants to collect and remit sales taxes to the state. The state then sued to enforce the law by naming online merchants such as Overstock.com and Newegg.com as defendants. The result of the state’s action was to produce a test case for the Supreme Court to potentially overturn its previous decisions.

The test case garnered enough attention that 35 other states joined in asking the Supreme Court to hear the appeal and potentially, overturn the rule. In addition to New York, the other states are: Alabama, Arkansas, California, Connecticut, Florida, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Kentucky, Maine, Maryland, Massachusetts, Michigan, Minnesota, Mississippi, Nebraska, New Mexico, North Carolina, North Dakota, Ohio, Oregon, Pennsylvania, Rhode Island, Tennessee, Texas, Utah, Vermont, Washington, Wisconsin, and Wyoming.The Court granted Certiorari to the State’s petition last week. You can read the Petition here.

Brick and Mortar retailers have also joined in urging the Court to hear the case. The National Retail Federation, the Retail Litigation Center, and the American Bookseller Association have all filed separate Amicus Curie briefs in support of South Dakota’s efforts.

Supporters of the 2016 law argue that the retail environment has changed so dramatically since the 1992 decision, that the rules set forth over 25 years ago need updating for the modern era. While few people would disagree with that premise, one of the original problems facing mail-order retailers in 1992 has not changed; there are thousands of individual sales tax jurisdictions, each with their own set of unique laws.

States and retailers will need to determine which sales tax laws should apply to the transaction. Should it be the billing address of the purchaser or the shipping address? What if an in-state purchaser has the product shipped to a different state? Where does the transaction actually occur?

Should the Supreme Court decide to overturn its prior decisions, it will add further uncertainty to the tax climate in the aftermath of the recent federal tax reform law.